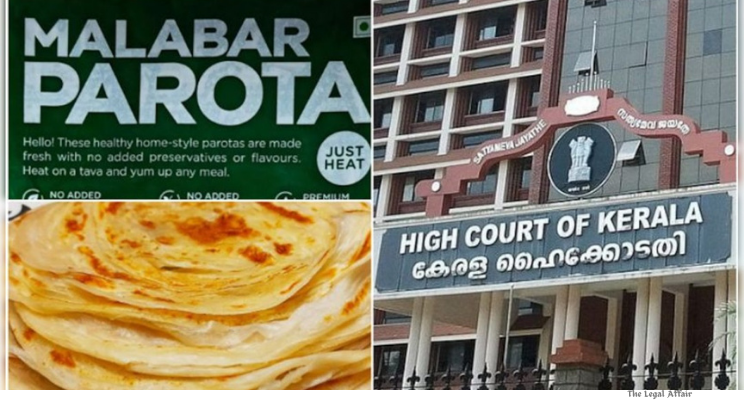

Introduction:

A recent decision by a Division Bench of the Kerala High Court has put on hold the classification of Malabar ‘Parota’ under the Goods and Services Tax (GST) regime, which was previously deemed eligible for a lower tax rate akin to bread. The case revolves around the interpretation of GST rates applicable to food products, specifically concerning Malabar Parota and Whole Wheat Malabar Parota.

Arguments of Both Sides:

Modern Food Enterprises Private Limited, the petitioner, sought a classification of its products, arguing that Malabar Parota qualifies as ‘bread’ and hence should be taxed at a lower rate of 5% under GST. They contended that their products, such as Classic Malabar Parota and Whole Wheat Malabar Parota, meet the criteria of bread under GST regulations.

The State Government, however, appealed against the single bench’s ruling that upheld the classification of Malabar Parota under the 5% GST category. The State argued that parotas, unlike bread, require additional processing before consumption and therefore do not fit the definition of bread under GST laws. This stance was supported by the Kerala Authority for Advance Ruling and Appellate Authority for Advance Ruling, which upheld an 18% GST rate for such products.

Court’s Judgement:

The Division Bench, comprising Justice A. Muhamed Mustaque and Justice S. Manu, stayed the operation of the single bench’s judgment for a period of two months pending further proceedings. The bench noted that the issue required deeper examination regarding the correct classification of Malabar Parota under the GST regime.

The bench’s decision effectively puts a hold on the application of the lower 5% GST rate on Malabar Parota, pending a comprehensive review of whether these products indeed qualify as ‘bread’ or fall under a higher GST rate category due to their specific characteristics and processing requirements.